ROI in Condominium Investments: A Complete Guide for Philippine Property Investors

In the Philippines’ fast-evolving property market, Return on Investment (ROI) isn’t just a nice-to-know figure—it’s the litmus test that separates profitable condominium deals from costly mistakes. With rising construction costs, fluctuating rental demand, and rapidly developing urban hubs, every peso invested needs to be measured against its potential to generate income or grow in value. For condo investors, ROI serves as the compass that points toward the most financially rewarding opportunities.

ROI plays a decisive role in determining whether to buy, hold, or sell a condominium unit.

Buy when the projected returns—whether from rental income, appreciation, or both—exceed market alternatives and justify the risks.

Hold if the property is delivering strong yields or positioned for significant value growth due to upcoming developments or market shifts.

Sell when ROI prospects plateau or decline, freeing up capital for better-performing investments.

Not all ROI is created equal. Condo investors typically fall into two main camps:

Capital Appreciation-Focused Investors – They play the long game, buying in emerging districts or pre-selling projects where value can climb significantly before resale. Here, ROI hinges on timing the market and capitalizing on location-driven growth.

Rental-Focused Investors – They prioritize steady cash flow, often targeting high-occupancy areas like BGC, Makati, or Cebu IT Park. For them, ROI is driven largely by rental yield, tenant stability, and cost management.

In practice, the most successful Philippine condo investors monitor both sides of the ROI equation—ensuring the property not only pays for itself through rentals but also builds substantial equity over time. This balanced view allows them to adapt their strategy to market changes and maximize overall returns.

Understanding ROI in Condominium Investments

Return on Investment (ROI) in real estate is the percentage measure of how much profit a property generates compared to its acquisition cost. In simpler terms, it answers the question: “For every peso I invest, how much am I getting back?” For condominium investors, ROI is the ultimate performance scorecard—it shows whether the property is financially worth holding or if capital should be redirected elsewhere.

The basic ROI formula looks like this:

This calculation hinges on two core components:

Rental Income / Rental Yield

Rental income is the money you receive from leasing out your unit, whether on a long-term lease or a short-term rental platform.

Rental yield expresses that income as a percentage of the property’s purchase price, providing a quick gauge of cash flow performance.

Example: If your Taguig condo rents for ₱35,000 per month (₱420,000 annually) and cost you ₱8,000,000, the gross rental yield is: (₱420,000 ÷ ₱8,000,000) \times 100 = 5.25\%

For a more realistic figure, investors calculate net rental yield by subtracting costs like association dues, property management fees, insurance, and taxes.

Capital Appreciation

This is the increase in your condo’s market value over time.

For example, if your unit’s value rises from ₱8,000,000 to ₱8,640,000 in one year, that’s an 8% appreciation—adding significantly to your ROI even without rental income.

Appreciation is driven by location demand, infrastructure projects, economic growth, and overall market sentiment.

The Time Horizon Factor

ROI isn’t static—it changes depending on how long you hold the property.

Short-term investors may prioritize high rental yields to recover costs quickly, often in established CBDs where rental demand is strong but appreciation is slower.

Long-term investors can afford to take lower immediate yields if they expect substantial appreciation over 5–10 years, especially in growth corridors like Clark, Bulacan, or emerging Metro Manila suburbs.

Smart investors assess ROI through both lenses—cash flow today and value growth tomorrow—ensuring that their condo not only covers its expenses but also compounds wealth over time.

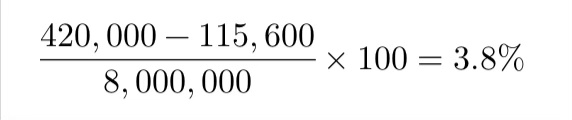

Evaluating Rental Yield

Rental yield measures the income-generating performance of a condominium relative to its purchase price. For Philippine condo investors, it’s one of the most telling metrics for understanding whether a property can sustain itself financially while delivering attractive returns.

Net Rental Yield: After ₱115,600 in annual costs → ₱304,400/year → 3.8%

This illustrates why investors should never stop at gross yield calculations.

Assessing Capital Appreciation Potential

Capital appreciation is the increase in a property’s market value over time. For long-term Philippine condo investors, it’s often the most powerful driver of wealth creation—sometimes dwarfing rental income in total returns. While rental yield keeps the cash flow steady, appreciation builds equity, which can be unlocked through refinancing or a profitable sale.

Why It Matters for Long-Term Investors

Capital appreciation compounds quietly in the background. A condo bought for ₱8,000,000 that grows at just 4% annually will be worth about ₱9,728,000 in five years—an unrealized gain of ₱1,728,000, even before rental earnings. When leveraged with financing, the percentage gain on your actual cash invested can be significantly higher.

Philippine-Specific Appreciation Drivers

1. Infrastructure Projects

Major transport upgrades tend to increase surrounding property values by improving accessibility.

Key examples:

Metro Manila Subway (connecting Quezon City to NAIA) expected to shorten travel times dramatically and increase demand in connected CBDs.

New Clark International Airport expansions boosting interest in Pampanga real estate.

North–South Commuter Railway improving connectivity between Metro Manila, Bulacan, and Pampanga.

2. Upcoming Business Hubs & Economic Zones

Areas designated as Special Economic Zones or targeted for IT-BPM expansionoften see rising demand for nearby residences.

Examples:

Bridgetowne East and West in Pasig-Quezon City boundary

Cebu IT Park expansion attracting more expats and local professionals.

3. Gentrification and Mixed-Use Developments

Redevelopment of underutilized areas into high-value, mixed-use communities drives price surges.

Bonifacio Global City’s transformation from a military base to a premium CBD is the textbook Philippine example.

Historical Data: Average Appreciation Rates

(Based on developer reports, Colliers, and Lamudi market snapshots)

Makati CBD: ~3–5% annually (mature market with stable demand)

BGC (Taguig): ~4–6% annually over the past decade, with faster growth in pre-2019 years due to rapid commercial build-out

Ortigas Center: ~3–4% annually, with potential uplift from Ortigas Greenways and Metro Manila Subway

Cebu IT Park: ~5–7% annually in peak years, driven by strong BPO presence and tourism spillover

How to Research Appreciation Potential

Check LGU Urban Development Plans

Local government websites often post zoning maps, road expansion projects, and infrastructure timelines.

Review Developer Track Record

Established developers like Ayala Land, SMDC, Rockwell Land have more consistent project delivery and value retention.

Analyze Demand-Supply Data

Look for reports from Colliers Philippines, Leechiu Property Consultants, JLL that track condo absorption rates and new supply pipelines.

Walk the Area

Observe ongoing construction, commercial activity, and lifestyle amenities. A neighborhood in transition often signals upward potential.

Example Projection: Taguig 1BR Condo

Purchase Price (Year 0): ₱8,000,000

Annual Appreciation Rate: 4%

Value After 5 Years: ₱8,000,000 \times (1 + 0.04)^5 = ₱9,728,000

Unrealized Gain: ₱1,728,000 (exclusive of rental income)

When paired with even a modest net rental yield of 3.8%, total ROI over five years becomes very competitive versus other investment classes.

Comprehensive ROI Analysis

To truly understand a condominium investment’s potential, you can’t just look at rental yield orcapital appreciation in isolation—you need to combine them into a total ROI calculation. This approach captures both the cash flow you earn and the equity growth your property gains over time.

Combining Rental Yield + Capital Appreciation

The total ROI formula is:

Total ROI (%)= Annual Net Rental Income + Annual Capital Appreciation/Purchase Price times 100

Example:

Purchase price: ₱8,000,000

Net rental yield: 3.8% → ₱304,400/year

Appreciation: 4% → ₱320,000/year

((₱304,400 + ₱320,000) / ₱8,000,000) times 100 = 7.8%

This means your property is generating the equivalent of 7.8% of its value in total returns each year—part in cash, part in equity growth.

Scenario Comparison

Different property types and locations have different ROI profiles:

High Yield, Low Appreciation

Common in tourist rentals in provincial cities (e.g., Siargao, Bohol)

You earn strong rental cash flow, but property values grow more slowly.

Low Yield, High Appreciation

Common in pre-selling units in CBDs (e.g., BGC, Makati, Cebu IT Park)

Rental income is modest initially, but the unit’s market value can rise quickly during construction and early turnover years.

ROI Sensitivity Analysis

Markets change, and so will your ROI. To avoid surprises, test your projections under different conditions:

Rental Vacancy: If occupancy drops from 95% to 80%, how much will your yield fall?

Maintenance Cost Spikes: Special assessments or major repairs can eat into profits.

Slower-than-Expected Appreciation: A projected 6% growth rate dropping to 3% over several years can dramatically affect returns.

By stress-testing your numbers, you’ll see how resilient your investment is in less-than-perfect conditions.

5-Year ROI Projection Table (Example: Makati 1BR Condo)

Scenario

Appreciation Rate

Net Rental Yield

Annual ROI

5-Year Total ROI

Best Case

6%

4.0%

10.0%

50.0%

Base Case

4%

3.8%

7.8%

39.0%

Worst Case

2%

3.0%

5.0%

25.0%

Interpretation:

Even in the worst case, the property remains profitable, though returns are more modest.

In the best case, the investment outperforms many fixed-income or stock market options in the Philippines.

Philippine-Specific Risks and How to Mitigate Them

Even the most promising condominium investment in the Philippines carries risks that can erode ROI if not addressed early. Understanding these challenges—and putting safeguards in place—can mean the difference between a thriving portfolio and a financial drain.

1. Market Volatility & Oversupply

The Risk: Certain areas, especially Metro Manila CBDs, can face periods of condo oversupply. When too many units hit the market at once—often from multiple pre-selling projects turning over simultaneously—rental rates stagnate or drop, and capital appreciation slows.

Mitigation:

Diversify your portfolio geographically (e.g., balance CBD units with emerging city investments like Iloilo, Davao, or Clark).

Prioritize properties in mixed-use communities where demand sources (residential, office, retail) are more stable.

Track absorption rates from reports by Colliers, Leechiu, or JLL to avoid overbuilt areas.

2. Regulatory Changes

The Risk: New government regulations can directly impact income potential. Examples include:

BIR enforcement on rental income tax (including stricter reporting and penalties)

Airbnb and short-term rental restrictions imposed by LGUs or building management associations

Mitigation:

Stay informed on tax policies by following BIR advisories and consulting with a CPA.

Structure leases to remain compliant—e.g., shift to mid-term (3–6 month) rentals if short-term bans tighten.

Invest in developments with clear, investor-friendly leasing policies in the master deed and house rules.

3. Association Dues & Special Assessments

The Risk: Condo ownership comes with monthly dues that fund maintenance and operations. These can rise sharply over time. Additionally, “special assessments” for major repairs (roof, elevator, façade) can hit without much warning.

Mitigation:

Ask for the condominium corporation’s audited financial statements before buying to check reserve fund health.

Favor developments with strong, transparent property management.

Factor at least 5–8% annual dues increase into your ROI projections to stay conservative.

4. Pre-Selling Delays & Turnover Quality Issues

The Risk: In the Philippines, pre-selling condos often face turnover delays due to construction, permitting, or financing problems. Even when delivered, some units require costly repairs or punch list work before they’re rentable.

Mitigation:

Choose developers with a strong delivery track record—Ayala Land, Rockwell, Alveo, DMCI are generally consistent.

Avoid buying in early project stages without a solid construction timetable and financing plan.

Negotiate turnover clauses that protect against excessive delay, or secure “ready-for-occupancy” units instead.

5. Disaster Risk (Flooding & Earthquakes)

The Risk: The Philippines is disaster-prone. Flooding, earthquakes, and typhoons can damage property, disrupt rental operations, and increase insurance costs.

Mitigation:

Check PHIVOLCS earthquake hazard maps and DPWH flood hazard maps before purchasing.

Prioritize developments with disaster-resilient design (e.g., elevated podiums, backup power, modern drainage).

Maintain comprehensive property insurance, including earthquake and flood coverage.

Stay updated, hire CPA, choose flexible leasing policy developments

Association dues increases

Review condo financials, factor escalations into ROI

Pre-selling delays

Buy from proven developers, secure clauses, consider RFO units

Disaster risk

Check hazard maps, choose resilient designs, get full insurance coverage

Leveraging Professional Help and Market Research

ROI in condo investing is rarely maximized by chance—it’s engineered through informed decisions and strategic execution. This is where industry professionals and credible market data become indispensable.

1. The Role of Licensed Real Estate Brokers in ROI Targeting

A seasoned, PRC-licensed broker does more than open doors to available units. They:

Identify high-yield neighborhoods and pre-market deals before they hit public listings.

Analyze recent comparable sales and rental rates to ensure you don’t overpay.

Provide insights on developer track records, which directly impacts long-term property value.

Assist in structuring purchase terms—payment schemes, discounts, or inclusions—that can improve ROI from day one.

Working with a broker who specializes in your target market (e.g., BGC, Makati, Ortigas) ensures your acquisition is both strategically located and financially viable.

2. How Property Managers Can Maximize Rental Income

A competent property manager isn’t just a caretaker—they’re an income optimizer. Their contributions include:

Setting market-aligned rental rates that avoid prolonged vacancies.

Coordinating repairs, staging, and marketing to maintain a competitive edge.

Handling tenant screening and contract compliance, reducing costly disputes or turnover.

Exploring alternative leasing strategies—such as mid-term rentals for expats or corporate leases—that may yield higher returns than standard one-year contracts.

For overseas Filipino investors, property managers act as the on-ground extension of their investment strategy.

3. Using Financial Advisors for Long-Term Investment Planning

A certified financial planner can help ensure your condo investments integrate smoothly with your broader wealth strategy by:

Advising on leverage and financing structures to minimize interest costs.

Planning for tax efficiency, especially if you have multiple income sources.

Mapping out reinvestment timelines—when to hold, refinance, or sell to redeploy capital.

This perspective prevents overexposure to one asset class and keeps your portfolio balanced.

4. Accessing Credible Market Data Sources

Your best investment decisions will be based on hard data, not just gut feel. Key sources include:

PSA (Philippine Statistics Authority) Housing Statistics::Tracks nationwide housing supply, construction trends, and demographic shifts—helpful in spotting underserved markets.

Colliers, Leechiu, and JLL Market Reports: Offer quarterly insights on rental yields, vacancy rates, absorption levels, and pipeline supply in specific districts. These are critical for timing purchases and avoiding oversaturated areas.

LGU Urban Development Plans: Local government master plans reveal where new infrastructure, transport links, or zoning changes will boost property demand—often years before the market catches on.

For overseas Filipino investors, property managers act as the on-ground extension of their investment strategy.

ROI-Boosting Strategies for Philippine Condo Investors

Maximizing returns in the Philippine condo market isn’t just about buying the right property—it’s about actively managing and repositioning that asset to outperform the average. The following strategies, when applied with precision, can significantly increase both rental yields and capital appreciation.

1. Renovations & Furnishing Upgrades for Higher Rent

In a competitive rental market, presentation is king. Even a modestly located unit can command premium rent with the right enhancements.

High-impact upgrades: Install modern lighting, upgrade kitchen fixtures, and add built-in storage solutions.

Tenant-focused furnishing: Target your tenant profile—corporate expats expect premium furniture and appliances, while young professionals value stylish but functional layouts.

Staging for ROI: Professionally staged photos and unit walkthroughs can justify a rental premium of 10–20% compared to unfurnished, basic units.

2. Switching from Long-Term Rental to Serviced Apartment Model

Shorter stays often yield higher per-night rates, especially in business hubs and tourist-favored cities.

Mid-term corporate leases: Secure 3–6 month stays from business travelers or project-based expats for steady cash flow without the churn of nightly rentals.

Tourism-driven stays: In areas like Makati, BGC, and Cebu IT Park, the serviced apartment model can outperform long-term leases by 30–50% if occupancy is maintained above 70%.

Hybrid approach: Keep flexibility—switch between long-term and short-term models depending on seasonal demand.

3. Timing Property Sales for Peak Demand

The same unit can yield vastly different profits depending on when it’s sold.

Watch supply cycles: Sell when competing inventory is low and new project turnovers are limited.

Leverage infrastructure projects: Properties near newly opened transport links or lifestyle hubs often experience sharp appreciation—ideal moments to exit.

Data-led timing: Use transaction data from Colliers or Lamudi to identify peak price seasons in your target area.

4. Negotiating Lower Acquisition Costs for Better Entry Yield

Your return starts the moment you buy. A lower acquisition cost not only improves your yield but also cushions against market dips.

Developer promos: Take advantage of pre-launch discounts, flexible payment schemes, or waived fees.

Distressed resales: Some sellers need fast liquidity—these can be acquired below market value.

Bulk or partnership buys: Pooling with other investors for multiple units can strengthen your negotiation position.

Sample ROI Calculator

Numbers tell the real story. To make ROI evaluation practical, let’s walk through a step-by-step computation using a real-world Philippine condo scenario.

ROI (%) = (Net Rental Income ÷ Total Acquisition Cost) × 100

ROI = (₱490,000 ÷ ₱7,400,000) × 100 = 6.62% annual ROI

Downloadable ROI Calculator

Conclusion & Next Steps

ROI analysis isn’t just a number-crunching exercise—it’s the investor’s reality check. In a market where glossy brochures and sales pitches can blur judgment, your ROI figure is the one metric that cuts through the noise. It tells you, in no uncertain terms, whether a condo is a cash machine or a cash drain. Without it, you’re essentially investing blind.

Every serious condo buyer in the Philippines—whether targeting steady rental income or long-term appreciation—should make ROI computation a standard part of their decision-making process. Use the formulas, track the numbers, and compare them across different properties. Even small percentage differences in ROI can translate to hundreds of thousands in additional returns over the life of your investment.

Now is the time to put this into action. Take the sample calculations from earlier in this guide and apply them to your own prospects. Test your assumptions. Play with the variables—rental rates, furnishing costs, association dues—to see how they impact the bottom line.

And if you want precision, speed, and professional insight, let me help you run the numbers. I offer a free personalized condo ROI report tailored to your target property and investment goals. No guesswork, no generic templates—just actionable, property-specific insights so you can buy, hold, or sell with confidence.

📩 Ready to see if your next condo deal makes the cut? Send me the property details, and I’ll deliver a full ROI breakdown straight to your inbox.

The Philippines boasts several prestigious residential properties, characterized by luxury, prime locations, and top-tier amenities. Notable addresses include Ayala Alabang… READ MORE

When buying a home in the Philippines, consider new constructions and resale properties. New homes offer customization, warranties, and modern… READ MORE

Leave a reply to Condominium Investment in the Philippines: How to Choose the Ideal Property – U-Property PH Cancel reply