You’ve come a long way—and you’re no longer just dreaming about homeownership. You’ve already laid the financial groundwork with a solid budget and loan pre-approval (as we tackled in Part 1), and you’ve spent the past few months exploring neighborhoods and touring promising properties (Part 2). Now, you’re entering a defining phase: narrowing down your top choices with precision and purpose.

At this point, it’s not just about what’s on the market. It’s about what aligns with your life, your goals, and your finances. You’re moving beyond browsing—and into the mindset of a serious, strategic buyer.

In Months 7 to 9, every decision becomes more intentional. You’ll evaluate lifestyle compatibility, long-term value, and the true cost of ownership. You’ll learn how to compare properties like a pro, negotiate with confidence, and prepare to make an offer that feels both bold and financially smart.

Whether you’re choosing between two dream homes or debating whether to walk away, this phase is about clarity and confidence. You’re not just picking a property. You’re choosing your future.

Let’s make it a decision you’ll never regret.

Evaluating Your Top Property Choices: How to Choose Wisely

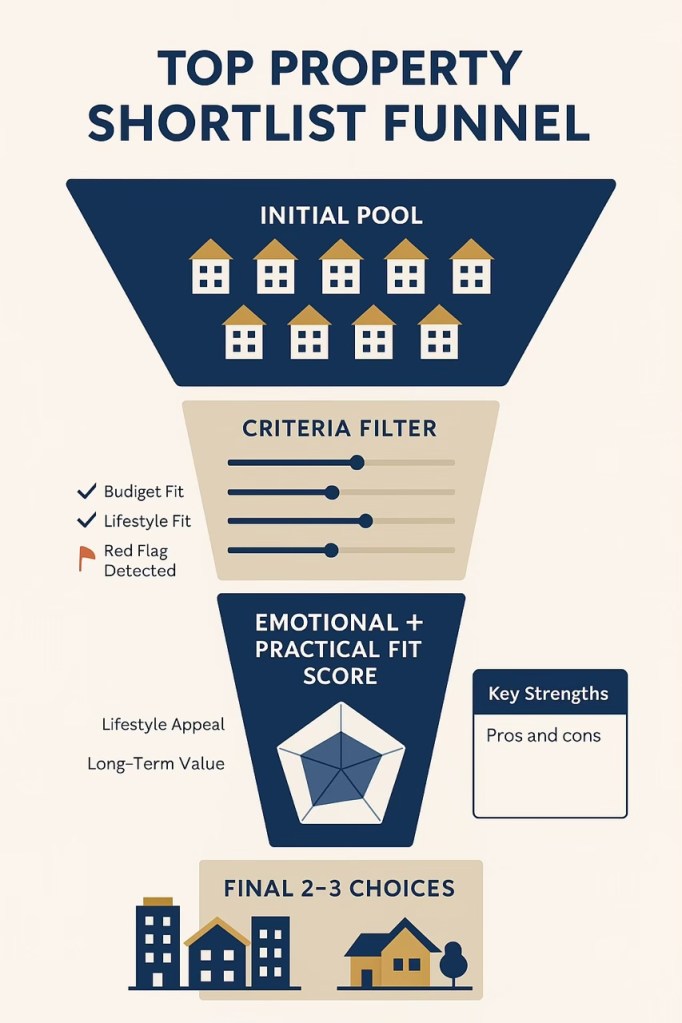

You’ve toured, taken notes, and felt the initial spark. Now comes the crucial step: evaluating your top properties with clear, practical criteria—not just emotions. Falling for a home is natural, but smart buyers weigh heart against hard facts. Here’s a comprehensive guide to making that decision razor-sharp and future-proof.

Lifestyle Fit: Can You See Yourself Living Here Daily?

Start with your day-to-day life. How long is your commute to work? Are quality schools nearby if you have or plan a family? What’s the public transport situation? Consider essentials like proximity to groceries, parks, hospitals, and gyms. No matter how stunning the home, a daily two-hour commute or inconvenient access can quickly drain your enthusiasm and budget.

Long-Term Potential: Think Beyond Today

A home isn’t just for now—it’s for your future. Will this property grow with your family or adapt to lifestyle changes? Investigate neighborhood trends: upcoming infrastructure projects, commercial developments, and community reputation. Homes in appreciating areas deliver stronger financial returns and stability. Don’t just buy a house—invest in a future-proof asset.

Property Pros and Cons: Inspect Every Detail

Evaluate each property with a critical eye. How functional is the layout? Is the floor area sufficient for your needs, or will it feel cramped soon? Inspect the condition of major systems—roofing, plumbing, electrical—and spot potential repairs or renovations. A fixer-upper can be a bargain, but only if you’re prepared for the time and cost investment.

Emotional vs. Practical: Balance Feelings With Facts

That perfect vibe—the warm lighting, the stunning balcony—can captivate, but don’t let emotional pull blind you to practical downsides like poor layout, high fees, or inconvenient location. List what excites you emotionally, then challenge each with practical questions. The best property balances both heart and head.

Pro Tip: Download our scoring matrix or comparison chart to keep your evaluation objective. Emotions fluctuate, but data drives smart decisions. See the download at the end of this article

Creating Your Final Shortlist: From 10 Options to the Top 2 or 3

This is the moment where clarity meets courage. You’ve done the groundwork—researched extensively, toured multiple properties, and analyzed the numbers. Now, it’s time to sharpen your focus and confidently trim your list to the top 2 or 3 properties that align perfectly with your goals, lifestyle, and budget.

Watch for Red Flags After Property Visits

What looked promising on the surface might hide costly issues beneath. Stay vigilant for warning signs like water stains, cracks in walls or ceilings, lingering strong odors (often masking problems), or homes that have lingered on the market with no price drops. These red flags demand deeper investigation—don’t let potential headaches sneak past your radar.

When to Trust Your Instincts and When to Dig Deeper

Your gut feeling is a powerful tool, but it must be balanced with facts. If a property sparks a strong “yes” or “no,” ask yourself why. Is it the ambiance, the view, or even the neighborhood vibe? If your instincts are based on vague discomfort, pause and analyze whether it’s emotional bias or a valid concern. Use concrete evidence to back up what your intuition tells you.

Revisit Your Top Contenders With Fresh Eyes

Second impressions often reveal what first visits miss. Schedule another visit at different times of the day to assess natural lighting, noise levels, and neighborhood activity. Bring along a trusted friend or family member for a fresh perspective—they might notice details you overlooked or confirm your findings.

Key Questions to Ask the Agent or Seller Before Finalizing Your Shortlist

Before committing any property to your final shortlist, get clear answers to critical questions:

| Why is the owner selling? Understanding motivation can guide your negotiation approach. |

| How long has the property been on the market? Extended listings may signal pricing or condition issues. |

| Have there been recent repairs, renovations, or inspections? This can affect your expected costs and timelines. |

| Are there any liens, easements, or legal complications tied to the title? These could delay or complicate ownership. |

| What’s the property’s value history over the last five years? Insight into appreciation trends helps assess investment potential. |

Be Ruthless—Your Future Depends on It

This isn’t just a choice of a home; it’s a strategic investment in your future. Cut loose properties that don’t meet your financial criteria or emotional needs. Only proceed with those that check all the essential boxes, blending practical value with personal fit.

The Art and Strategy of Negotiation: Don’t Just Accept the Price

Negotiation isn’t about confrontation or luck—it’s a disciplined skill that can save you hundreds of thousands of pesos or add significant value to your real estate purchase. The listed price? Almost never set in stone. When you’re making one of the biggest investments of your life, mastering negotiation is non-negotiable.

How to Determine a Fair Offer

Begin with data, not guesses. Conduct a comparative market analysis (CMA) by reviewing recent sales of similar properties in the area to set a realistic offer baseline. Adjust for the property’s current condition—consider needed repairs, outdated finishes, or structural issues. Next, uncover the seller’s motivation. Are they eager to sell fast? Have they already bought another home? Sellers under pressure give you leverage to negotiate a better deal.

Proven Negotiation Tactics That Work

- Anchoring: Start with an offer slightly below your target price. This sets the negotiation tone and gives you room to move.

- Contingencies: Include protective clauses like “subject to financing approval” or “pending home inspection” to safeguard your interests while signaling commitment.

- Offer Speed and Certainty: Sellers value quick closings, flexible move-in dates, or larger earnest money deposits—even if your offer isn’t the highest. These can be powerful bargaining chips.

When to Walk Away

Not every negotiation ends in success. Recognize these red flags: inflexible pricing despite glaring flaws, vague or evasive answers about legal documents, or pressure to decide before reviewing paperwork. If you feel trapped or uneasy, step back. The right property is out there—don’t settle for a bad deal.

Real Talk: Filipinos and Negotiation Culture

Many Filipino buyers hesitate to negotiate, fearing it might offend. But here’s the truth: polite assertiveness is expected and respected in real estate transactions. Negotiation isn’t about being difficult; it’s about being informed, professional, and firm on what’s fair. You can maintain respect while protecting your investment.

Sample Negotiation Dialogue

| Buyer: “We’re very interested, but based on recent comparable sales and the necessary kitchen and plumbing repairs, we’d like to offer ₱6.5 million instead of ₱6.8 million.” |

| Seller’s Agent: “The seller is hoping for the full asking price.” |

| Buyer: “We understand, but we’re ready to move quickly and cover processing fees if we can agree on ₱6.5 million. Given the market and repairs, we believe this is a fair offer.” |

Simple, calm, and strategic—no drama, just results.

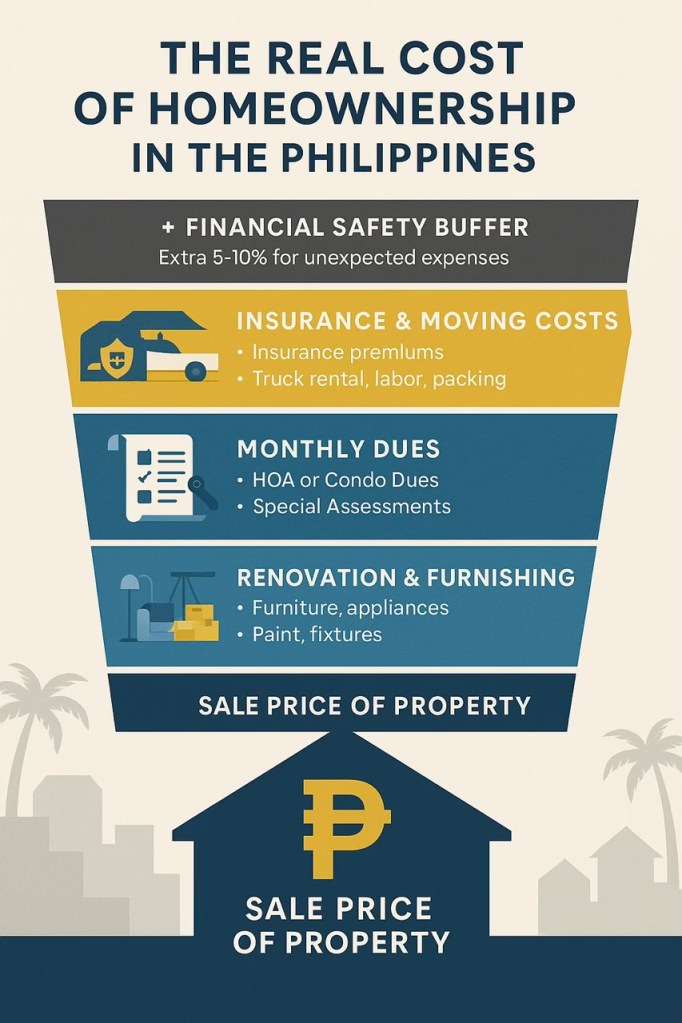

Budgeting for the True Cost of Ownership: Beyond the Sale Price

Focusing solely on the property’s sale price is a rookie mistake. The real financial commitment kicks in after your offer is accepted. Extra costs—often overlooked—can tack on an additional 5% to 10% (or more) of the purchase price. Smart buyers plan for these upfront to avoid surprises and secure true financial peace of mind.

Transfer Taxes, Notarial Fees, and Title Registration Costs

In the Philippines, transferring property ownership involves mandatory government fees that you must budget for:

- Documentary Stamp Tax (DST): Typically 1.5% of the higher amount between selling price or zonal value.

- Transfer Tax: Usually ranges from 0.5% to 0.75%, depending on the local government unit.

- Registration Fee: Around 0.25% of the selling price to register the title.

- Notarial Fees: Normally between 1% and 2% of the selling price for the notarization of contracts.

If the seller isn’t covering these costs, prepare to shoulder them. These fees are non-negotiable and must be paid to legitimize your ownership.

Homeowner Association (HOA) Dues or Condo Fees

Monthly dues are often underestimated but can seriously impact your budget. These fees cover security, maintenance of common areas, waste disposal, and shared amenities. Depending on the property—whether a subdivision or condominium—fees can range from a few hundred pesos to several thousand monthly. Always ask for exact dues and watch out for special assessments that can spike costs unexpectedly.

Renovation and Furnishing Costs

Even “move-in ready” homes usually need tweaks or upgrades. Think repainting walls, replacing fixtures, upgrading countertops, or custom cabinetry. Don’t forget furniture essentials: appliances, beds, air conditioning units, curtains, and lighting. Budget at least ₱200,000 to ₱500,000 for mid-range renovations and furnishings. If you want full customization or high-end finishes, costs will climb.

Insurance and Moving Expenses

Protect your investment with fire and property insurance—often required by lenders if you’re using financing. Insurance premiums are relatively affordable but recurring. Moving costs—truck rental, labor, packing materials, and possible temporary storage—add up quickly, especially if relocating across cities or islands. Factor these into your initial budget.

The Bottom Line

The purchase price is just the starting line. True homeownership comes with layered expenses that can derail unprepared buyers. By planning for taxes, fees, renovations, insurance, and moving costs ahead of time, you eliminate financial surprises and gain confidence in your investment.

Mini Milestone Checklist (Months 7–9)

This is the critical middle stretch of your home buying journey. If you’ve ticked off most of these milestones, you’re steering confidently toward success. This phase demands clarity, solid strategy, and confidence. Use this checklist to verify you’re making smart, informed decisions—no guesswork, just progress.

📋 Mini Milestone Checklist: Months 7–9

| ✅ Compared at Least 3 Top Properties |

|---|

| Evaluated each for lifestyle fit (location, commute, amenities) and long-term financial value (resale potential, market trends). |

| ✅ Narrowed Down to Top 2–3 Choices |

|---|

| Clearly defined the pros and cons for each contender to maintain objectivity and focus. |

| ✅ Researched Recent Sales and Market Data |

|---|

| Used recent sales and pricing trends to set a realistic negotiation baseline. |

| ✅ Set a Maximum Offer Budget |

|---|

| Included hidden costs like taxes, HOA fees, renovation estimates, and insurance. |

| ✅ Confident to Initiate Negotiation |

|---|

| Prepared a fair, well-reasoned offer—and ready to walk away if needed. |

Progress: 80% Complete

What’s Next: Making the Offer & Closing the Deal (Months 10–12)

You’ve laid the foundation. The research, comparisons, tough decisions, and negotiation practice have set the stage. Now comes the pinnacle of your journey: making the offer, sealing the deal, and stepping confidently into your new home.

In this final phase of your 12-month home buying plan, you’ll get clear, actionable guidance on every critical step:

- Submitting a Formal Offer with Confidence: Craft a compelling, well-reasoned offer that reflects your research and budget—showing you mean business

- Handling Counteroffers & Price Negotiations: Navigate back-and-forth offers smoothly, knowing when to stand firm and when to compromise.

- Conducting Thorough Due Diligence: Verify legal documents, confirm a clean and transferable title, and carefully review contract terms to protect your investment.

- Coordinating with Banks, Brokers, and Legal Experts: Align all parties for seamless processing of loan approvals, document signings, and compliance requirements.

- Preparing for Your Move-In: Organize logistics, set up utilities, and plan your transition so your new home welcomes you without a hitch.

This final chapter transforms your months of preparation into true ownership. We’ll ensure you close with confidence, clarity, and no second-guessing. The keys are within reach—let’s finish strong and unlock your future.

Want to Choose the Right Property Without Second-Guessing?

You’re almost there—and we’ve built a tool to help you finish strong.

Get our FREE Property Evaluation Matrix, a powerful yet simple scoring system that helps you compare your top 2–3 home options with clarity and objectivity. Designed for Filipino homebuyers, this matrix includes local cost considerations, lifestyle metrics, and negotiation-readiness checkpoints.

| 📋 Use it to: |

|---|

| ✔️ Compare properties side-by-side |

| ✔️ Avoid emotional decision-making traps |

| ✔️ Budget realistically beyond the sale price |

| ✔️ Know when to move forward—or walk away |

📩 Once you sign up, your free matrix will land in your inbox—ready to guide your next property decision like a pro.

Smart buyers don’t guess. They evaluate.

Leave a comment