Introduction – What Just Happened?

Two powerful storms — Typhoon Kalmaegi (local name: Tinio) and Super Typhoon Fung-Wong (local name: Uwan) — slammed into the Philippines in quick succession, putting the nation’s resilience to its toughest test yet. Within a single week, torrential rains, storm surges, and landslides swept across Luzon and the Visayas, leaving thousands of homes damaged, roads impassable, and investors anxiously watching how the country’s property market would react.

Entire neighborhoods were submerged. Power and water outages crippled major cities. Construction sites ground to a halt as materials and manpower were diverted toward recovery efforts. From flooded subdivisions in Pampanga and Bulacan to condominium towers in Metro Manila grappling with basement leaks and power interruptions, the blows were widespread and costly.

For homeowners, these back-to-back typhoons served as a sobering reminder that climate resilience isn’t optional — it’s essential to protecting both family and financial stability. For developers, it was a stress test of design integrity, flood-mitigation systems, and post-disaster response. And for investors, the message was unambiguous: climate risk is now investment risk.

This article explores how the twin typhoons are reshaping Philippine real estate — from the immediate physical and financial impact on homes and condos to the market’s short-term reactions and the emerging strategies for building climate-smart portfolios in a country on the front line of extreme weather.

Why the Philippines Is Uniquely Vulnerable

Geographical & Meteorological Factors

The Philippines sits squarely on nature’s front line. Positioned in the Northwest Pacific Basin, it sees approximately 20 tropical cyclones entering its area of responsibility each year, many making landfall. Coupled with over 7,000 km of coastline and a terrain filled with low‑lying plains, steep slopes and river systems, the stage is set for compound risk: wind, storm surge, heavy rainfall, flooding and landslides.

Rapid urbanisation intensifies the threat. More than half the population now lives in cities — many of which cling to coastlines or rivers. A recent World Bank analysis found major Philippine cities disproportionately exposed to typhoon‑ and flood‑related damage because of poor land‑use planning and informal settlements. Climate change is turning up the heat. Intensifying storms, rising seas and wetter extreme events mean that what was once a “storm every few years” scenario is now much more frequent and severe.

From a real‑estate perspective, that means properties are not just assets — they are high‑exposure assets. If your condo is near a riverbank in Metro Manila or your subdivision is in a low‑lying coastal barangay, the odds of facing storm‑related disruption are materially higher.

Historical Storm‑Impact on Property

The figure speak plainly. Since 1990 the Philippines has endured 565 major disaster events, with damages totaling approximately US $23 billion and nearly 70,000 lives lost. A landmark case: Typhoon Haiyan (Yolanda, 2013) — the strongest storm to make landfall in recorded Philippine history — damaged over 1.1 million homes and shattered infrastructure across nine regions.

In the real‑estate world, that translates into delays, cost overruns, diminished asset values, and heightened insurance and maintenance costs. For instance:

- Entire development pipelines get delayed because roads, bridges or power supply are damaged after a typhoon.

- Sub‑divisions in flood‑prone zones can suffer value erosion when buyers perceive higher ongoing risk.

- Insurance premiums for properties in typhoon “hot zones” are higher and sometimes harder to secure. According to investment commentary, areas such as Eastern Visayas, Bicol and Northern Luzon are already seeing this pressure.

When investors assume property markets in the Philippines behave like “calm” markets, they underestimate how quickly a natural‑hazard event can reset expectations about location, risk and asset liquidity.

Immediate Impact on Homes and Residential Real Estate

The back-to-back strikes of Typhoon Kalmaegi (Tino) and Typhoon Fung-Wong (Uwan) have delivered a sharp, immediate shock to the Philippine housing and residential real estate market. From low-density suburban subdivisions to high-rise condominiums, no segment was untouched, and the ripple effects are already shaping buyer sentiment, developer strategies, and investor confidence.

Detached Houses & Suburban Homes

Suburban and rural homes bore the brunt of floodwaters, landslides, and wind damage. In provinces like Cebu, Bulacan, and Bicol, low-lying subdivisions experienced severe inundation, with many homes reporting partial structural damage or compromised foundations. Roofs were blown off older homes, and wooden structures were particularly vulnerable.

Homeowners now face not only repair costs but also disrupted access to their properties due to washed-out roads and damaged bridges. For property investors and homeowners, these events highlight the critical importance of elevation, drainage planning, and storm-resilient constructionin risk-prone areas.

Condominiums & High-Rise Units

High-rise and mid-rise condominiums in Metro Manila and other urban centers faced a different spectrum of challenges. While structural integrity largely held, lobbies, parking basements, and lower floors experienced flooding, and power and water outages disrupted daily operations. Some developments reported elevator shutdowns and temporary suspension of amenities, causing inconvenience for tenants and short-term rental losses.

Investors in condo units are now evaluating flood mapping, basement protection, and emergency response protocols as a core part of due diligence, particularly for properties marketed as “premium” or “resilient.” Developers are also recalibrating marketing and insurance strategies to emphasize disaster readiness.

Infrastructure & Utilities Hit (Key for Value Retention)

The typhoons didn’t just impact buildings—they disrupted critical infrastructure and utilities that underpin property value. Roads, bridges, drainage systems, and local power grids suffered extensive damage. Substations and water supply lines were compromised, leaving entire neighborhoods temporarily uninhabitable or inaccessible.

For residential real estate, the lesson is clear: property value is inseparable from functional infrastructure. A well-built home in a flood-prone area loses market desirability if access and utilities are unreliable. Investors are increasingly scrutinizing municipal drainage systems, flood barriers, and emergency response plans when assessing long-term value.

Effects on the Investment Property Market

The twin typhoons—Kalmaegi (Tinio) and Fung-Wong (Uwan)—have not only battered homes and condos but are already sending shockwaves through the Philippine investment property market. From short-term rental losses to shifts in resale pricing and delayed development pipelines, the storms are forcing investors, developers, and market watchers to recalibrate risk assumptions and investment strategies.

Rental Properties: Short-Term Shocks

For rental properties, the immediate impact is tangible. Flooded basements, damaged access roads, and intermittent power and water supply have temporarily displaced tenants, resulting in lost rental income for landlords. Short-term rental markets in flood-prone areas such as Pasig, Marikina, and low-lying provinces in Central Luzon are seeing cancellations, delayed move-ins, and reduced occupancy rates.

Landlords and property managers are now prioritizing storm resilience measures—elevated units, emergency backup power, and insurance coverage—to maintain tenant confidence. Investors are learning the hard way that climate risk translates directly into cash flow risk.

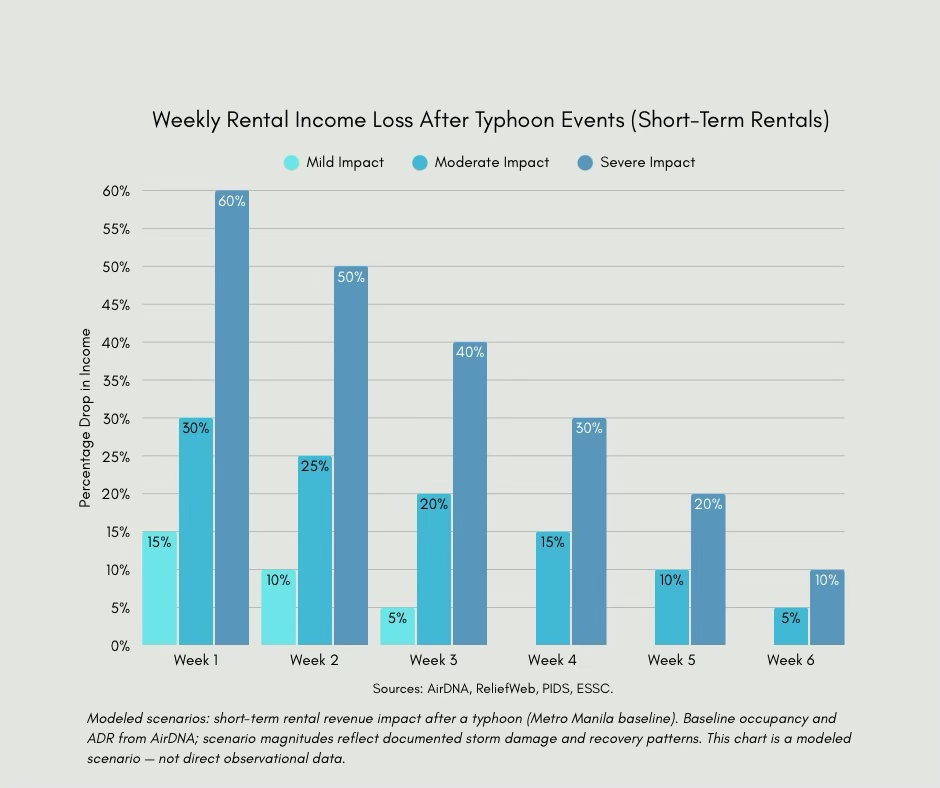

This chart illustrates how short-term rental income typically declines in typhoon-affected areas of the Philippines, depending on the severity of the event. In mild-impact zones, earnings recover quickly after a brief 15%–10% drop, while moderate-impact areas experience a 30%–25% decline that takes up to six weeks to normalize. Severe-impact zones—often hit by flooding or infrastructure disruptions—can see income plunges of up to 60% in the first week, with a slower rebound over more than a month. The data highlights the importance of insurance coverage, risk mapping, and cash-flow buffers for property investors operating in high-exposure regions.

Resale Market: Risk Perception & Pricing Adjustments

Typhoon exposure is recalibrating resale valuations across affected regions. Buyers are increasingly wary of properties in flood-prone or poorly drained areas, while developers and brokers must contend with perceived risk dampening demand.

Early data from affected provinces indicate that subdivision in flood-prone barangays often experience slower resale demand and downward pricing pressure following major typhoons, while high-rise condos with resilient infrastructure tend to maintain value, albeit with higher insurance and maintenance considerations. Investors must now factor in storm frequency, historical damage, and municipal response when assessing long-term resale value.

Developer Pipeline & Project Delays

For developers, the typhoons are causing logistical and financial disruptions. Construction timelines are delayed as building materials, equipment, and labor are redirected to emergency recovery. Active sites in Luzon and Visayas face stalled operations due to flooding, unstable ground conditions, and supply chain interruptions.

These disruptions carry cascading effects: delayed turnover dates, postponed sales launches, and added costs for storm-proofing measures. Investors must now assess project timelines against climate risk exposure and adjust expectations for returns accordingly.

Regional & Asset-Type Comparison

The impact of Typhoon Kalmaegi (Tinio) and Typhoon Fung-Wong (Uwan) has varied significantly depending on location, property type, and age of construction. Understanding these distinctions is critical for homeowners, investors, and developers aiming to navigate the Philippine real estate market amid increasing climate risks.

Metro Manila / NCR vs. Provincial Coastal & Typhoon-Prone Areas

Metro Manila and the National Capital Region (NCR

Urban high-density areas experienced flooding in low-lying districts, basement inundation in condominiums, and power and transport interruptions. While high-rise buildings largely withstood wind damage due to stricter building codes, older structures and subdivisions near rivers and esteros remain vulnerable.

Provincial Coastal & Typhoon-Prone Areas

Regions such as Eastern Visayas, Bicol, and Northern Luzon faced the most severe impacts. Homes built on low-lying floodplains or steep slopes suffered structural damage, washouts, and landslides. Access to properties was disrupted, delaying recovery and amplifying short-term market uncertainty.

Key Takeaway: Urban centers benefit from infrastructure and code enforcement, but provincial and coastal properties carry higher exposure risk, affecting both occupancy and investment value.

New Developments vs. Older Stock

New developments

Often incorporate modern storm-mitigation features: elevated ground floors, reinforced structures, better drainage, and flood-resistant landscaping. These measures reduce physical damage and help preserve property value, though they can increase insurance premiums.

Older stock

Particularly pre-2010 homes and condominiums, tends to be more vulnerable to flooding, roof damage, and compromised utilities. Many older subdivisions were built before stricter local building codes or climate-resilient planning requirements were enforced.

Key Takeaway: Age of construction is a critical determinant of storm resilience and future-proofing, making it a core factor in risk assessment and investment planning.

Flood-Prone Zones, Landslide Zones, Storm-Surge Zones

Typhoon impact is not uniform even within a single province or city. Risk exposure is influenced by topography, proximity to coastlines or rivers, soil stability, and municipal infrastructure.

Flood-prone zones

Low-lying urban districts or river-adjacent subdivisions. High water levels can damage basements, ground floors, and roads.

Landslide zones

or mountainous areas with unstable soil, often affecting rural and semi-urban properties.

Storm-surge zones

Coastal barangays and islands vulnerable to sea-level rise and high tide during typhoons.

Understanding these micro-risks allows homeowners, investors, and developers to align property selection, insurance, and mitigation strategies with actual hazard exposure.

Comparative Risk Table: Property Types & Regional Exposure

| Asset Type / Region | Flood Risk | Landslide Risk | Storm-Surge Risk | Structural Vulnerability | Notes for Investors / Buyers |

|---|---|---|---|---|---|

| Metro Manila High-Rise Condo | Moderate | Low | Low | Low | Elevators & basements susceptible; newer buildings fare better |

| Metro Manila Older Suburban Homes | High | Low | Low | Moderate | Prone to street flooding; insurance recommended |

| Provincial Coastal Subdivision Homes | High | Low | High | Moderate to High | High exposure to storm surge; roof and flood mitigation critical |

| Provincial Hilly/Rural Properties | Moderate | High | Low | Moderate | Landslide mitigation and site grading essential |

| New Development Condos/Subdivisions | Moderate | Low | Low to Moderate | Low | Built with modern codes; resilient design reduces damage risk |

| Older Development Condos/Subdivisions | High | Low | Low to Moderate | Moderate | May require retrofitting and flood-prevention upgrades |

Warning Signs & Red Flags for Investors and Home Buyers

Typhoons like Kalmaegi (Tinio) and Fung-Wong (Uwan) highlight a hard truth: not all properties are created equal when it comes to climate resilience. For homeowners and investors, identifying warning signs early can mean the difference between a secure asset and a financial liability.

1. Structural Damage Potential

A property’s construction quality is the first line of defense against extreme weather. Warning signs include:

Aging structures

Homes or condos built before modern typhoon-resilient codes (pre-2010) are more vulnerable to roof damage, foundation cracks, and wall collapse.

Inferior materials or workmanship

Substandard concrete, unreinforced masonry, or improperly installed roofing dramatically increase repair costs after storms.

Visible cracks or water intrusion

Even minor signs can indicate long-term vulnerability to flooding and wind damage.

Investor Tip: Always request building plans, certification of structural inspections, and past maintenance records to assess true resilience.

2. Flood/Landslide History and Local Micro-Risk

Location is everything. Properties in areas with a documented history of flooding, landslides, or storm surge exposure carry amplified risk. Critical considerations:

Historical flooding data

Check municipal flood records, river/estero overflow histories, and past storm impact reports.

Soil and topography

Slopes, reclaimed land, or low-lying zones significantly increase exposure.

Micro-risk variability

Even within the same subdivision or city, small differences in elevation or drainage can determine whether a property floods or stays dry.

Investor Tip: Use geospatial tools, hazard maps, and government flood zone data to evaluate micro-risk before purchase.

3. Insurance, Maintenance, and Infrastructure Resiliency

A resilient property isn’t just about the structure—it’s about services, upkeep, and contingency planning. Red flags include:

Limited or expensive insurance coverage

High premiums or exclusion clauses for typhoon damage indicate elevated risk.

Deferred maintenance

Slopes, reclaimed land, or low-lying zones significantly increase exposure.

Fragile utility and access infrastructure

Properties dependent on unreliable roads, power grids, or water supply may suffer operational disruption even if the building survives.

Investor Tip: Use geospatial tools, hazard maps, and government flood zone data to evaluate micro-risk before purchase.

4. Over-Leveraged Developments and Project Delays

Not all developments weather typhoons equally. Red flags in the investment pipeline include:

Financially over-leveraged developers

Projects with stretched cash flow may struggle to repair storm damage promptly or complete construction on time.

Chronic delays

Previous delays in turnover, infrastructure completion, or amenity delivery may indicate underlying project fragility.

Lack of disaster preparedness

Developments without storm mitigation systems—elevated structures, drainage retention, or backup utilities—are high-risk for investors and buyers alike.

Investor Tip: Review developer track records, verify completion timelines, and demand evidence of storm-resilient planning before committing capital.

How to Protect Yourself / Best Practices

In the wake of Typhoon Kalmaegi (Tinio) and Typhoon Fung-Wong (Uwan), the Philippine real estate market has made one truth crystal clear: prevention, preparedness, and proactive evaluation are non-negotiable. Homeowners, condo buyers, and investors can protect their assets by adopting evidence-backed strategies, aligning with best practices, and using verifiable data to guide decision-making.

For Homeowners: Mitigation, Maintenance, Contingency Planning

1. Structural and Landscape Mitigation

- Reinforce roofs, walls, and foundations using typhoon-resilient materials.

- Elevate critical utilities and install flood barriers where feasible.

- Maintain proper drainage and grading around your property to redirect water flow.

2. Regular Maintenance

- Inspect roofs, gutters, and downspouts seasonally.

- Repair cracks in walls, windows, or foundations before heavy rainfall seasons.

- Keep landscaping trimmed and remove debris that can block water flow.

3. Contingency Planning

- Maintain an emergency kit and evacuation plan for all family members.

- Have clear communication lines and insurance claims protocols ready.

- Document property condition with photos for insurance and legal purposes.

For Condo Purchasers / Renters: Building Credentials, Neighborhood Risk, Elevation / Flood Line

1. Verify Building Credentials

- Check developer reputation, compliance with Philippine Structural Code, and building permits.

- Request evidence of typhoon- and flood-resistant features such as elevated basements, reinforced concrete cores, and resilient glazing.

2. Assess Neighborhood Risk

- Examine historical flooding, storm-surge, and drainage patterns in the immediate vicinity.

- Confirm municipal or barangay disaster response capabilities and infrastructure reliability.

3. Check Elevation and Flood Lines

- Higher-floor units generally face lower flood risk but may be more exposed to wind.

- Confirm that the building is above local flood lines and that lower levels have adequate waterproofing and drainage.

For Investors: Due-Diligence Checklists, Stress-Testing, Exit Strategy

1. Comprehensive Due Diligence

- Analyze developer history, insurance coverage, structural integrity, and prior storm performance.

- Evaluate municipal infrastructure, including roads, drainage, power, and water reliability.

2. Stress-Test Rental and Resale Scenarios

- Model worst-case scenarios for rental income loss during typhoon season.

- Consider resale impact for properties in flood-prone or landslide-vulnerable zones.

3. Develop an Exit Strategy for High-Risk Zones

- Identify alternative markets or properties with better resilience.

- Ensure liquidity and contingency reserves are sufficient for emergency repairs or temporary vacancies.

Expert Insights & Data — What the Numbers Say

Bridging the gap between theory and action, this section draws from credible studies and industry observations to present the hard data underpinning the impact of typhoons on the Philippine property market. Facts first—then the real estate implications you need to understand.

Number of Typhoons & Frequency

- The Philippine Atmospheric, Geophysical and Astronomical Services Administration (PAGASA) and affiliated sources report that the Philippines sees an annual average of approximately 19.5 typhoons making landfall or affecting the country across recent decades.

- While the number of storms hasn’t risen dramatically, their intensity and destructive potential are increasing. Recent analysis shows stronger winds and heavier rainfall per event.

- One summary states the Philippines receives “about 18 to 20 typhoons per year” across the Philippine Area of Responsibility (PAR).

With nearly two dozen storm events annually, many of which cause flooding or landslides, you cannot treat disaster risk as an outlier. It’s intrinsic.

Typical Damage Costs in the Philippines

- Annual damage from typhoons in the Philippines has been estimated at ₱30 billion to ₱80 billionacross sectors in recent years.

- One research compilation indicates repair costs for individual residential properties in risk zones can span ₱100,000 to ₱500,000 per major storm event, depending on location and construction quality.

These cost ranges translate into meaningful risk premiums for properties. Buyers and investors in high‑exposure zones must factor in extra maintenance, repair and eventual de‑valuation risk.

Research on Housing Vulnerability Index for Typhoon Hazards

- A 2023 article titled “A census‑based housing vulnerability index for typhoon hazards in the Philippines” developed a municipal‑level index from 25 census‑based indicators (housing quality, crowding, tenure security, structural integrity, etc.).

- The research found systematic spatial patterns: vulnerability increased in certain municipalities, indicating that not just broad geography but local housing conditions significantly determine risk.

You’re not just buying in the “right city”—you need to evaluate the housing vulnerability profile of the micro‑location. This index offers a framework for risk‑scoring properties or developments.

Synthesis & Implications for Real Estate

- Frequency × cost × vulnerability = risk multiplier: Frequent typhoons, high repair/maintenance costs and localized housing fragility together escalate real‑estate risk in exposed zones.

- Location + quality matter more than ever: A well‑constructed property in a lower‑vulnerability municipality may fare far better than a poorly maintained house in a high‑exposure area.

- Insurance and investor vigilance will rise: Given the cost benchmarks and vulnerability data, premiums, due diligence and investor expectations will shift accordingly—you’ll see this in pricing, exit‑strategies and lenders’ requirements.

- Market differentiation expects resilience: As the data becomes more accessible (via indices, hazard maps, repair‑cost benchmarks), properties will increasingly be categorized not just by location and amenities—but by storm resilience and recovery profile.

Case Studies & Anecdotes

Real data and statistics provide authority, but real stories drive understanding and engagement. These case studies illustrate how typhoons like Kalmaegi (Tinio) and Fung-Wong (Uwan) play out in real estate—from individual homeowners to large-scale investors—demonstrating both vulnerability and resilience.

1. Homeowner in Bicol Region: Rebuilding After Typhoon Damage

Profile

A family-owned detached house in Legazpi City, Albay, built in the early 2000s on slightly elevated land but without modern storm mitigation features.

Impact

- Roof partially blown off and walls cracked due to strong winds.

- Flooding reached 30–50 cm inside the ground floor, damaging furniture and appliances.

- Access roads were blocked, delaying emergency aid and construction materials delivery.

Recovery & Lessons

- The family invested in reinforced concrete roofing, elevated utilities, and improved drainage.

- Reconstruction took approximately 4–6 months, longer than anticipated due to supply chain delays and labor shortages.

- Insurance coverage partially offset repair costs, highlighting the importance of comprehensive typhoon insurance.

2. Condo Development in Metro Manila: Minimal Damage Through Resilience

Profile

A mid-rise condominium in Makati City, completed in 2018, designed with storm-resistant construction standards, elevated parking basements, and reinforced windows.

Impact

- Ground-level lobbies and parking areas experienced minor flooding due to heavy rain, but units remained unaffected.

- Power outage lasted less than 24 hours thanks to backup generators, maintaining tenant comfort.

- Amenities like gyms and pools temporarily closed, but no structural damage was reported.

Investor & Developer Lessons:

- The development’s modern design and infrastructure minimized downtime and protected long-term asset value.

- High-quality construction translated into investor confidence, with no significant drop in resale or rental demand post-typhoon.

- Developers highlighted emergency response protocols, drainage capacity, and structural reinforcement as key differentiators in marketing resilience.

3. Investor Holding Property in a Typhoon-Prone Zone

Profile

A mid-rise condominium in Makati City, completed in 2018, designed with storm-resistant construction standards, elevated parking basements, and reinforced windows.

Impact

- One unit experienced minor flooding; tenant temporarily relocated.

- Repair costs were moderate due to pre-installed flood barriers and elevated electrical systems.

Strategy & Lessons

- Investor maintained a contingency fund and comprehensive insurance, allowing rapid repairs and minimal income disruption.

- Tenant relations were proactively managed through transparent communication and temporary relocation support, preserving long-term rental confidence.

- Post-event analysis led the investor to stress-test potential acquisitions using municipal flood maps and vulnerability indexes before purchase.

Conclusion / Key Takeaways

The recent twin typhoons—Kalmaegi (Tinio) and Fung-Wong (Uwan)—underscore a non-negotiable reality: the Philippine real estate market is highly exposed to natural disasters, and resilience is now a core investment criterion. From Metro Manila high-rises to provincial coastal homes, the combination of location, construction quality, infrastructure, and preparedness dictates both short-term damage and long-term asset value.

Key Takeaways for Homeowners, Buyers, and Investors:

- Geography and micro-location matter – Flood-prone, landslide-vulnerable, and storm-surge zones carry the highest risk, even within the same city or subdivision.

- Age and quality of construction are critical – Modern developments built to typhoon-resistant codes withstand storms far better than older stock.

- Insurance and contingency planning are indispensable – Comprehensive coverage and emergency protocols mitigate financial losses and disruption.

- Investors must stress-test assumptions – Rental and resale income projections should account for climate risk, repair costs, and delayed turnovers.

- Data-driven evaluation is essential – Use hazard maps, vulnerability indexes, and historical storm impact data to guide purchasing and investment decisions.

- Resilient properties maintain value – Properties with reinforced structures, reliable utilities, and proactive mitigation measures recover faster and sustain rental/resale demand.

By understanding these principles, readers can make informed, strategic decisions that safeguard assets and optimize long-term returns in a climate-risk environment.

Take Action

The twin typhoons—Kalmaegi (Tino) and Fung-Wong (Aghon)—have made one thing clear: proactive measures are essential to protect your real estate investments in the Philippines. Whether you own a home, are planning to buy a condo, or manage an investment portfolio, taking decisive action now can safeguard your property value and minimize risk.

For Homeowners: Protect Your Family and Property

Schedule a Property Risk Assessment

Identify structural vulnerabilities, flood exposure, and drainage issues before the next typhoon season.

Implement Mitigation Measures

Reinforce roofs, elevate utilities, and maintain proper drainage to reduce storm damage.

For Condo Buyers & Renters: Choose Safety with Confidence

Request proof of typhoon-resistant design, building code compliance, and flood protection measures.

Check Neighborhood Risk

Review local flood, landslide, and storm-surge history before committing.

For Investors: Protect Capital and Maximize Returns

Create a Typhoon-Resilient Due-Diligence Checklist

Assess developer track records, infrastructure, and market risk.

Stress-Test Rental and Resale Scenarios

Model potential impacts of typhoons on income and property value to make informed investment decisions.

Leave a comment