(Featuring a Real-Life Example: Maria’s Journey to Homeownership Through Bank Financing)

Embarking on the journey to buy your first home in the Philippines is an exciting prospect, often coinciding with other significant life events. If you’re a Filipino breadwinner navigating this milestone, you might be exploring the best financing options available.

This guide focuses on bank financing as a viable and often preferred route for first-time homebuyers in the Philippines. We’ll follow the experience of Maria*, a 30-year-old Filipina earning ₱90,000 monthly, as she considers purchasing her dream ₱5 million home near her mother, primarily looking at bank loan options. By understanding Maria’s situation and the intricacies of bank home loans, you’ll gain valuable insights into your own path to homeownership.

Disclaimer: Maria’s name has been changed to protect her privacy, but her situation reflects the realities faced by many young Filipino professionals.

Decoding Affordability: Maria’s Financial Snapshot

Let’s examine Maria’s current financial standing to assess her readiness for homeownership through bank financing:

| Financial Detail | Amount |

|---|---|

| Monthly Income | |

| Monthly Salary | ₱75,000 |

| Passive Income | ₱15,000 |

| Total Monthly Income | ₱90,000 |

| Savings & Assets | |

| Emergency Fund | ₱500,000 |

| Downpayment Saved | ₱1,000,000 |

| Monthly Saving Capacity | ₱35,000 – ₱40,000 |

| Target Property | |

| Target Property Value | ₱5,000,000 |

| Target Loan Amount | ₱4,000,000 |

Initial Assessment: With a strong ₱1 million downpayment and a comfortable ₱500,000 emergency fund, Maria is in a favorable position to pursue a bank home loan. The key question remains: Can she sustainably manage the monthly mortgage payments and associated costs with a bank loan? Let’s investigate further.

Crunching the Numbers: Can Maria Afford the Monthly Amortization with a Bank Loan?

The monthly mortgage payment is a significant factor when considering bank financing. Here’s a breakdown of potential mortgage options for Maria’s ₱4 million loan from various banks:

| Term | Estimated Interest Rate | Monthly Payment | Potential Lender(s) |

|---|---|---|---|

| 30 years | 7.25% (Bank A) | ₱27,470 | Major Banks (e.g., BPI) |

| 25 years | 7.00% (Bank B Promo) | ₱28,300 | Security Bank, other promos |

| 20 years | 7.50% (Bank C) | ₱32,210 | Metrobank, UnionBank |

| 15 years | 8.00% (Bank D) | ₱38,280 | Various Banks |

Important Note: Interest rates for bank home loans can vary significantly based on the bank, loan term, your credit score, and prevailing market conditions. It’s crucial to shop around and compare offers.

The Debt-to-Income (DTI) Ratio: Assessing Affordability with Bank Financing

The Debt-to-Income (DTI) ratio is a crucial metric used by banks to evaluate your loan repayment capacity:

- Ideal Housing DTI: Banks generally prefer a housing DTI below 30% to 35% of your gross monthly income.

Let’s calculate Maria’s housing DTI based on the 30-year loan option from Bank A:

- Maria’s Housing DTI: ₱27,470 (Monthly Payment) ÷ ₱90,000 (Total Monthly Income) = 30.5%

Analysis: Maria’s housing DTI is within the generally acceptable range for bank financing. This suggests she can likely manage the monthly payments while still having funds for other expenses.

Addressing Key Concerns: Emergency Fund, Baby Plans, and Wedding Costs (with Bank Financing in Mind)

Maria’s concerns about her emergency fund and future plans remain valid when considering bank financing:

Furniture and House Essentials:

The Challenge: Furnishing costs can be substantial, and Maria wants to preserve her ₱500,000 emergency fund.

| The Solution: |

|---|

| ✅ Personal Loan Options: Some banks offer personal loans with competitive interest rates that Maria could explore for furniture and appliance purchases, rather than solely relying on her emergency fund. |

| ✅ Credit Card Installment Plans: Utilizing 0% installment plans offered by credit cards for appliances and furniture can be a smart strategy. |

Having a Child Soon:

The Challenge: Anticipated monthly expenses for a baby (₱10,000 – ₱15,000) need to be factored in.

| The Solution: |

|---|

| ✅ With a manageable monthly mortgage payment (around ₱27,000 – ₱28,000 based on the longer-term options), Maria has more flexibility in her budget to accommodate these upcoming childcare costs. |

Wedding Expenses:

The Good News: As with the Pag-IBIG scenario, Maria’s wedding fund of ₱1 million is separate from her home-buying savings, preventing any financial conflict.

Your Roadmap to Homeownership: Navigating Bank Home Loan Options

Understanding the landscape of bank home loans in the Philippines is essential for first-time buyers. Here’s a closer look:

Exploring Bank Home Loan Promos:

Major banks frequently offer attractive home loan promotions. Keep an eye out for:

| BPI Home Loan | Known for its various loan packages and online application options. |

| Metrobank Home Loan | Often features competitive interest rates and flexible payment terms. |

| Security Bank Home Loan | Offers a range of loan products and may have specific promotions for first-time buyers. |

| UnionBank Home Loan | Provides digital application processes and various financing solutions. |

| Other Banks | Don’t overlook other reputable banks like RCBC, PNB, and EastWest Bank, as they may also have appealing offers. |

Pro Tip for First-Time Buyers: When comparing bank offers, always inquire about the total cost of the loan, including interest rates, processing fees, appraisal fees, legal fees, and mortgage redemption insurance (MRI). Some banks may offer bundled packages or fee waivers as part of their promotions.

Budgeting for Homeownership with Bank Financing: Upfront and Ongoing Costs

Be prepared for these costs associated with bank financing:

| Expense Type | Estimated Cost | Important Tips |

|---|---|---|

| Closing Costs | ₱150,000 – ₱250,000 | This can include bank processing fees, appraisal fees, documentary stamp tax, transfer tax, registration fees, and notary fees. Budget accordingly. |

| Taxes & Insurance | ₱5,000 – ₱7,000/month | Often bundled with your monthly mortgage payment (including property insurance and Mortgage Redemption Insurance). Confirm with your bank. |

| Furniture & Appliances | ₱150,000 – ₱300,000 | Explore personal loans or credit card installment plans to manage these expenses without depleting your emergency fund. |

| Childcare Expenses | ₱10,000 – ₱15,000/month | Factor this into your long-term budget projections. |

Your Step-by-Step Guide to Securing Your First Home with Bank Financing

Following Maria’s lead, here’s a practical plan for securing your dream home through a bank loan:

Step 1: Assess Your Financial Readiness and Loan Eligibility

- Review your income, savings, and existing debts to determine how much you can comfortably afford for a monthly mortgage.

- Check your credit score, as this will significantly impact the interest rates you’ll be offered.

Step 2: Shop Around and Compare Bank Offers

- Research different banks and their home loan packages online.

- Visit at least 2-3 banks to inquire about their specific rates, fees, and requirements.

- Ask for a detailed breakdown of all costs involved in the loan.

- Inquire about pre-approval processes.

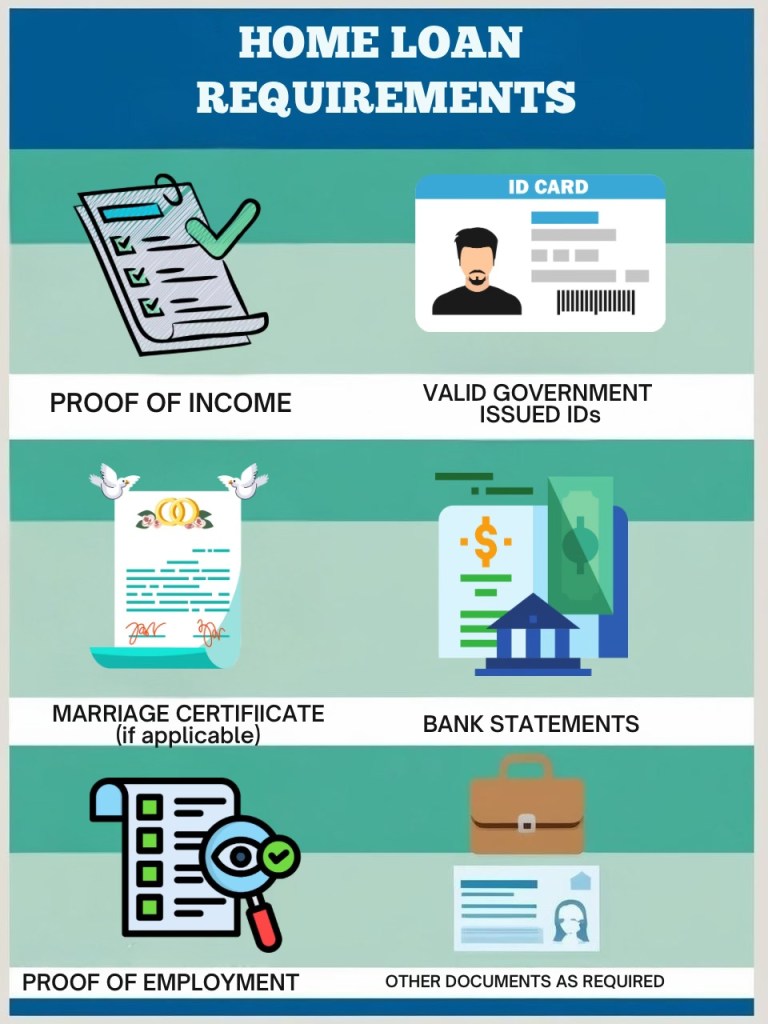

Step 3: Gather Required Documents

Step 4: Obtain Bank Pre-Approval

- Getting pre-approved for a home loan will give you a clearer idea of the loan amount you qualify for and strengthen your position when making an offer on a property.

Step 5: Submit Your Loan Application and Complete Requirements

- Once you’ve chosen a bank, submit your complete loan application along with all necessary documents.

- Cooperate with the bank during the appraisal process for the property you intend to purchase.

Step 6: Review and Sign the Loan Agreement

- Carefully review all the terms and conditions of the loan agreement before signing. Don’t hesitate to ask for clarification on anything you don’t understand.

Step 7: Pay Closing Costs and Secure Your Home

- Once the loan is approved, you’ll need to pay the closing costs.

- The bank will then process the release of the loan, and you can finalize the purchase of your dream home.

Step 8: Plan Your Move and Enjoy Your New Home!

- Coordinate your move-in and start making your new house a home.

The Verdict: Is Bank Financing the Right Path for You?

Yes, for many first-time homebuyers like Maria, bank financing offers a reliable and accessible route to homeownership in the Philippines. With careful research, comparison of offers, and sound financial planning, securing a bank home loan can turn your dream into a reality.

Maria’s situation demonstrates that with a solid downpayment, a steady income, and a realistic budget, navigating bank financing is a viable option.

Key Takeaways for Aspiring Filipino Homebuyers Considering Bank Financing:

✅ Bank Financing is a Popular Option: Many Filipinos successfully achieve homeownership through bank loans.

✅ Compare Offers Diligently: Interest rates and fees can vary significantly between banks, so thorough comparison is crucial.

✅ Understand All Costs: Be aware of all upfront and ongoing costs associated with a bank home loan.

✅ Get Pre-Approved: This step provides clarity on your borrowing capacity and strengthens your offer.

✅ Maintain a Good Credit Score: A good credit history can help you secure better interest rates.

Ready to Take the Next Step Towards Your Dream Home with Bank Financing?

If you’re considering bank financing for your first home in the Philippines, remember that you have numerous options available. Take the time to research, compare, and understand the process. With careful planning and the right bank partner, your dream of owning a home near your loved ones can become a reality.

Let’s discuss your bank financing options, explore suitable properties, or help you navigate the bank loan application process. You might be closer to your dream home than you think!

Leave a comment